Research, Evidence & Performance

A Strategy Built Through Research, Testing, and Verification

What you see today is the result of more than a year of systematic research into sports market inefficiencies.

Before capital was deployed, we focused on data quality, robustness, and repeatability, not short-term results.

Our objective was simple but demanding:

Build a strategy that remains profitable across time, across market conditions, and across inevitable variance.

1. Research, Analysis & Methodology

Data Collection & Preparation

Historical match data and pricing across multiple leagues and seasons

Full normalization of results into a consistent, bet-level dataset

Focus on net outcomes, not headline win rates

Strategy Exploration

Multiple strategy variants were tested, including:

Different market types

Alternative signal filters

Varying stake allocation methods

Conservative vs aggressive execution rules

Each iteration was evaluated on:

Expected value

Drawdown behavior

Sensitivity to variance

Stability across time windows

Only strategies that survived strict robustness filters were retained.

2. Why This Strategy Survived When Others Did Not

Many strategies look attractive in isolated samples.

Most fail when exposed to:

Different months

Changing market liquidity

Unfavorable sequencing of results

The final strategy was selected because it demonstrated:

Positive expectancy across large samples

Controlled drawdowns under realistic assumptions

Resilience to adverse run distributions

This is a process-driven selection, not result-driven cherry-picking.

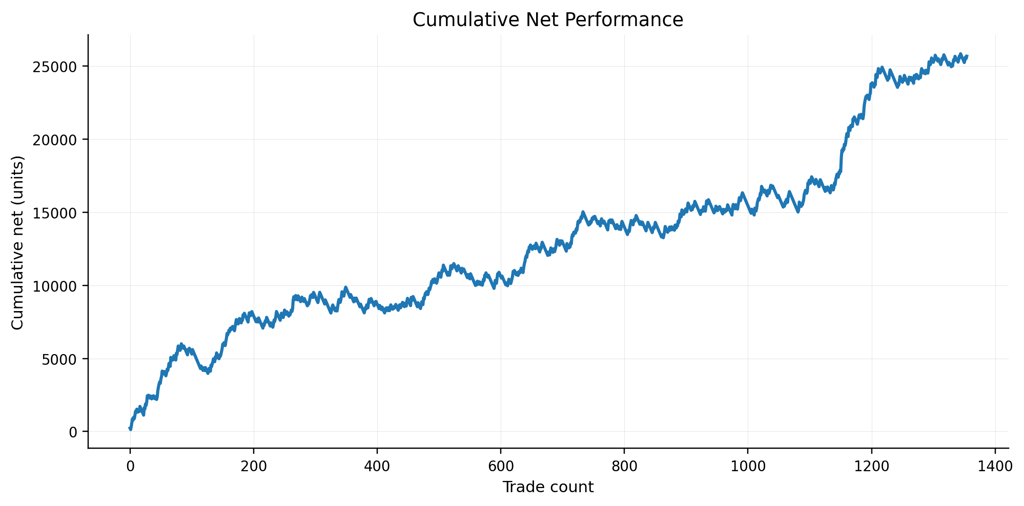

This chart shows the cumulative net result derived from historical trade data, using a fixed reference stake per trade. Results are presented for informational purposes only and reflect past observations. Past performance is not indicative of future results.

3. Historical Performance Applied Retrospectively

Back-Application to the Previous Year

The final version of the strategy was applied to last year’s data as if it had been running live, using:

Fixed, rule-based execution

No hindsight adjustments

No parameter tuning after the fact

This produced:

Consistent profitability across the year

Expected short-term volatility

Clear evidence of long-term edge

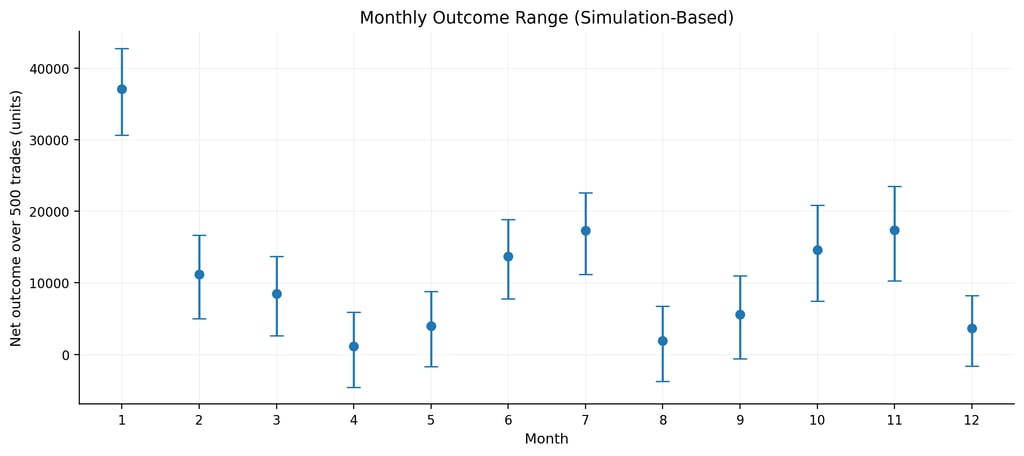

4. Understanding Variability: Good Months and Bad Months

Short-term variability is unavoidable in any probabilistic strategy.

To address this honestly, we analyzed performance by calendar month and by rolling periods, rather than relying on annual aggregates.

Key findings:

Some months consistently outperform

Some months introduce higher variance

Annual performance is not dependent on perfect monthly consistency

This is expected in a statistically sound system.

This chart summarises simulation-based estimates of outcomes over a fixed number of trades, analysed independently for each calendar month. Results are derived from resampling historical trade outcomes and are intended to illustrate variability and seasonality. Extreme upside outcomes have been excluded to avoid distortion.

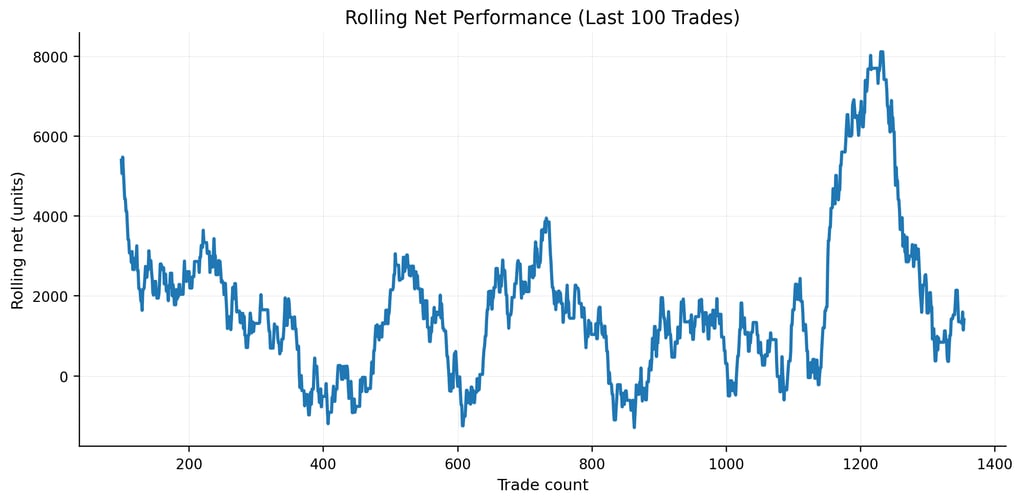

Rolling net results calculated over a fixed number of trades illustrate short-term variability and drawdowns that may occur during normal operation of the strategy. Periodic fluctuations are expected in probabilistic trading systems

5. Monte Carlo Analysis: Stress-Testing the Strategy

To move beyond historical sequencing, we applied Monte Carlo simulations to the strategy.

What We Tested

We simulated 10,000 different “years”, where each year consists of:

1,000 trades

Fixed stake of 100 units per trade

Trades are drawn from the historical distribution of real results

No leverage, no compounding assumptions

Each simulation represents a plausible alternative year, not a forecast

Why Monte Carlo Matters

Historical results show what happened once.

Monte Carlo shows what can reasonably happen many times.

This allows us to:

Estimate realistic return ranges

Quantify drawdown probabilities

Understand capital stress scenarios

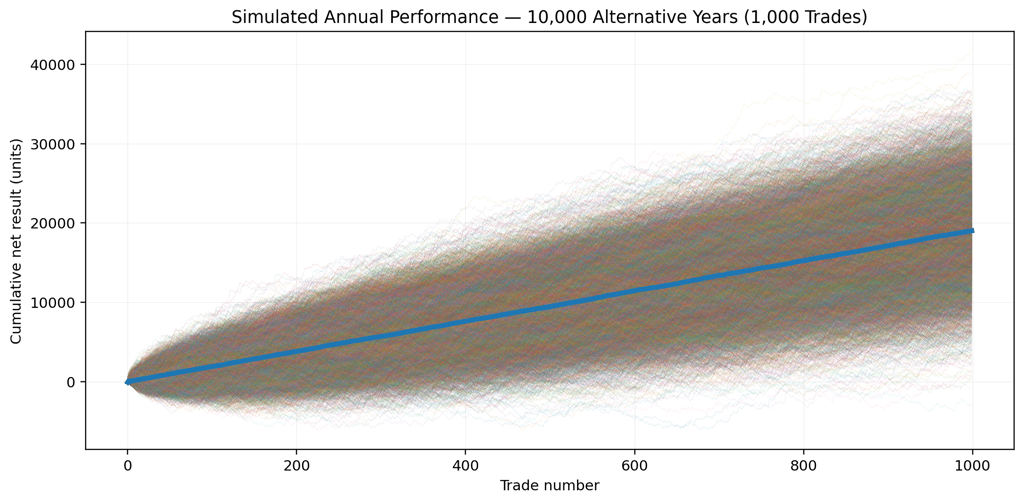

Each thin line represents a simulated annual performance path generated by re-sequencing historical trade outcomes over a fixed number of trades. The bold line represents the median outcome across all simulations. This analysis is intended to illustrate potential variability of results under different trade sequences and does not constitute a prediction of future performance.

6. Annual Perspective: Why the Strategy Works Over Time

The strategy is not designed to “win every month”.

It is designed so that:

Strong months more than compensate weaker ones

Profitable periods compound faster than losses detract

Capital growth is driven by edge + discipline, not leverage

Typical annual outcomes remain strongly positive

Variance smooths over sufficient sample sizes

Conservative stake sizing materially reduces capital stress

7. Ongoing Monitoring & Governance

Research does not stop at deployment.

The strategy is continuously monitored for:

Deviation from expected behavior

Structural changes in market conditions

Risk concentration across time or leagues

Adjustments are made only when justified by data, not short-term outcomes.